How to compare lender quotes on commercial real estate deals

How to compare lender quotes on commercial real estate deals. Terms to track, how to normalize across lenders, and the mistakes that cost basis points.

14-day free trial · Full access · Cancel anytime

Used by commercial real estate investment and development teams to manage deals from sourcing to close.

Why lender comparison is harder than it should be

Every commercial real estate financing conversation starts with a deceptively simple task: compare the lender quotes and pick the best one. In practice, this task is where otherwise organized deal teams lose hours every week to manual reconciliation, and where small errors can cost tens of basis points on multi-year loans. A 10 basis point mistake on a $30 million ten-year loan is around $300,000 over the life of the loan. These are real dollars, and the process that produces them is unstructured.

The first issue is that lender quotes are not standardized. Every lender has its own term sheet format, its own way of presenting the rate (base plus spread, all-in, or indicative), its own amortization structure, its own prepayment terms, and its own covenant language. One lender quotes a ten-year term with thirty-year amortization, 65 percent LTV, and a soft step-down prepay. Another quotes a seven-year term with IO for five years, 70 percent LTV, and a yield maintenance prepay. A third quotes ten years with no IO, 60 percent LTV, and a flat 1 percent exit fee. These quotes are not directly comparable, and making them comparable requires normalizing them into a common framework.

The second issue is that quotes evolve. A lender sends an initial indicative quote. The deal team provides more information. The lender comes back with a revised quote. The team negotiates on rate or LTV. The lender issues a final term sheet. By the time the financing decision is made, each lender might have sent three or four distinct quotes, each with slightly different terms, each of which needs to be tracked and compared. A spreadsheet that holds one row per lender cannot represent this history, and most teams resort to keeping the term sheets as PDFs in a folder and comparing them manually.

The third issue is that the comparison is not just about the quoted rate. The effective cost of the loan depends on the rate, the amortization structure, the prepayment terms, the origination fee, the exit fee, any servicing or collateral requirements, the covenants, and the expected exit strategy. A lower rate with a painful prepay might be more expensive than a higher rate with a soft step-down. Most teams do not quantify this explicitly, which means they are making the decision on partial information.

The fourth issue is traceability. Three months into a ten-year loan, the team needs to reference what the original lender quotes said, how the final term sheet compared, and why the chosen lender was picked. If the comparison was done on a spreadsheet that has been overwritten, the history is lost. This is a problem for auditing, for learning, and for the next time the team needs to solicit quotes on a similar deal.

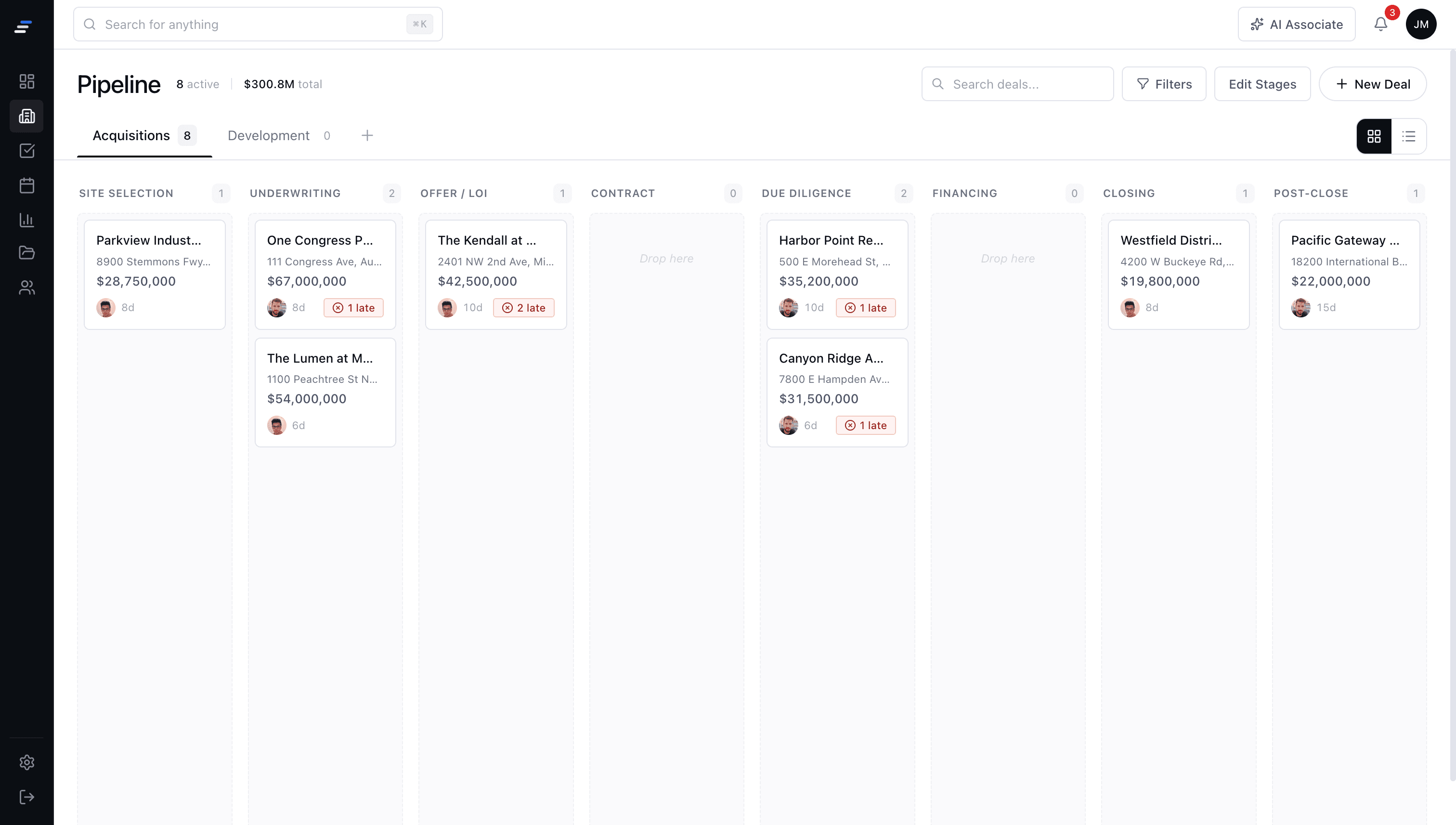

Pipeline

A CRE pipeline, done right

Every deal has a workspace, every workstream has an owner, and the pipeline is a live view into the team's actual work.

How to run a lender comparison that catches the real costs

A strong lender comparison captures four things: the quoted terms, the history of quotes from each lender, the normalized effective cost, and the non-rate factors that affect the decision.

1. Track every quote, not just the latest one

Keep every version of every quote from every lender. When a lender comes back with a revised term sheet, add it as a new entry and preserve the previous one. This lets the team see how the negotiation evolved and gives the principal a factual record to reference later.

2. Normalize the terms into a common framework

Put the quotes into a common table with the same columns for each: rate (all-in), rate basis (fixed, floating, hedged), amortization, IO period, term, LTV, DSCR requirement, origination fee, prepay structure, exit fee, recourse, and covenants. The normalization exposes the differences that matter.

3. Calculate the effective cost

Use the same discount methodology for each lender to compute the effective all-in cost of the loan, assuming the team's expected hold period and exit strategy. The lender with the lowest quoted rate is not always the lender with the lowest effective cost. Prepay penalties and exit fees can shift the answer.

4. Score the non-rate factors

Rate is not the only factor. Speed of execution, relationship value, flexibility on covenants, and lender reputation during the closing process all matter. Score these explicitly (even if subjectively) so the comparison does not collapse into a one-dimensional rate comparison.

5. Preserve the decision rationale

Write down why the chosen lender was chosen. Not just 'lowest rate,' but the specific combination of factors. This becomes a reference for future deals and a training artifact for newer team members.

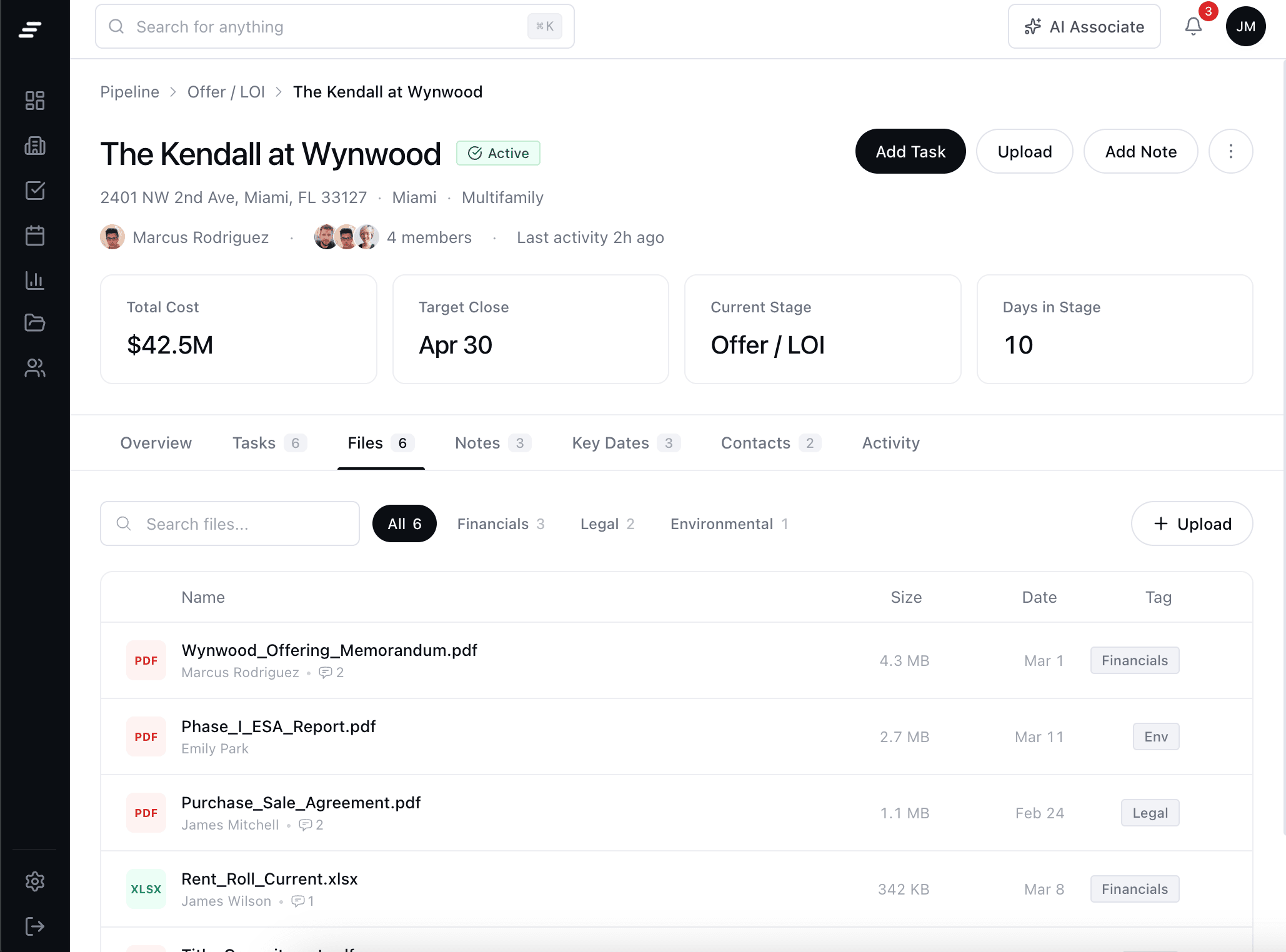

How MotionCRE tracks lender quotes on every deal

MotionCRE includes a financing tracker as part of every deal workspace. Each lender conversation is captured as a set of quotes, with the ability to add new quote versions as the negotiation evolves. The tracker shows every lender side by side with normalized terms: rate, amortization, LTV, DSCR, prepay structure, and fees.

When the team is ready to make a financing decision, the side-by-side view supports the comparison directly. No spreadsheet rebuilding, no PDF shuffling, no hunting for the latest term sheet. The decision rationale gets written into the workspace notes, and the full history stays with the deal permanently for auditing and learning.

When you need to share the deal package with a lender, deal rooms let you grant access to the relevant documents (OM, rent roll, T-12, inspection reports) with an audit trail. The lender sees only the files you want them to see, access is revocable, and you know exactly what they have opened.

Common questions

Every quote should be normalized across rate (all-in), amortization, IO period, term, LTV, DSCR, origination fee, prepayment structure, exit fee, recourse, and covenants. The team should also score non-rate factors like execution speed and relationship value, and compute a normalized effective cost for the expected hold period.

Join CRE teams already running their deals on MotionCRE

Your pipeline, your deals, tracked from sourcing to close.

14-day free trial · Full access · Cancel anytime