IC memo template for commercial real estate deals

A practical IC memo template for commercial real estate acquisition teams. Structure, required sections, and the fields investment committees actually ask about.

14-day free trial · Full access · Cancel anytime

Used by commercial real estate investment and development teams to manage deals from sourcing to close.

What an IC memo is actually for

The IC memo is the document that asks your investment committee to approve a deal. It summarizes the opportunity, the underwriting, the risks, and the recommendation. The committee reads it (or skims it) and decides whether to commit capital, pass, or ask for more work. On the surface, the memo is a piece of writing. In practice, it is a forcing function for the deal team. The act of writing a good IC memo surfaces gaps in the underwriting that would otherwise stay hidden until due diligence or closing.

Most IC memos fail in one of three ways.

The first failure mode is that the memo is written as a sales pitch. The deal team is emotionally committed to the deal by the time the memo is being written. The committee reads an eight-page narrative about why this is a great opportunity and why the team loves the asset. The memo avoids or downplays risk. The committee either approves based on a one-sided view (and finds out about the risks during DD) or pushes back hard and the team has to rewrite the memo under pressure. Either outcome is worse than if the memo had been honest from the start.

The second failure mode is that the memo is built from the spreadsheet instead of from the workspace. The analyst builds the underwriting model, exports the key metrics, and writes a memo around those numbers. The problem is that the memo lives in a Word doc and the model lives in Excel. When the model updates (and it always does), the memo goes stale. The team ends up with a memo that references numbers the model no longer contains, and the committee asks 'is this the latest' at the top of the meeting, and the answer is 'let me check.'

The third failure mode is that the memo does not reflect the DD work. By the time the memo is being written, the team has done weeks of inspections, lender conversations, environmental reviews, and legal reviews. The memo should summarize what those workstreams found. But because the memo is written in isolation from the deal workspace, the author has to manually recreate the DD narrative from emails and notes. Things get missed. The committee asks about an environmental issue that surfaced two weeks ago and was never written into the memo.

The underlying problem is that the memo is treated as a document instead of as a live view into the deal's state. The memo should assemble itself from the workspace: the economics come from the model, the DD findings come from the workstream tasks, the financing terms come from the financing tracker, and the risks come from a running decisions log. When the memo is a view instead of a copy, it stays current and the committee gets a consistent story.

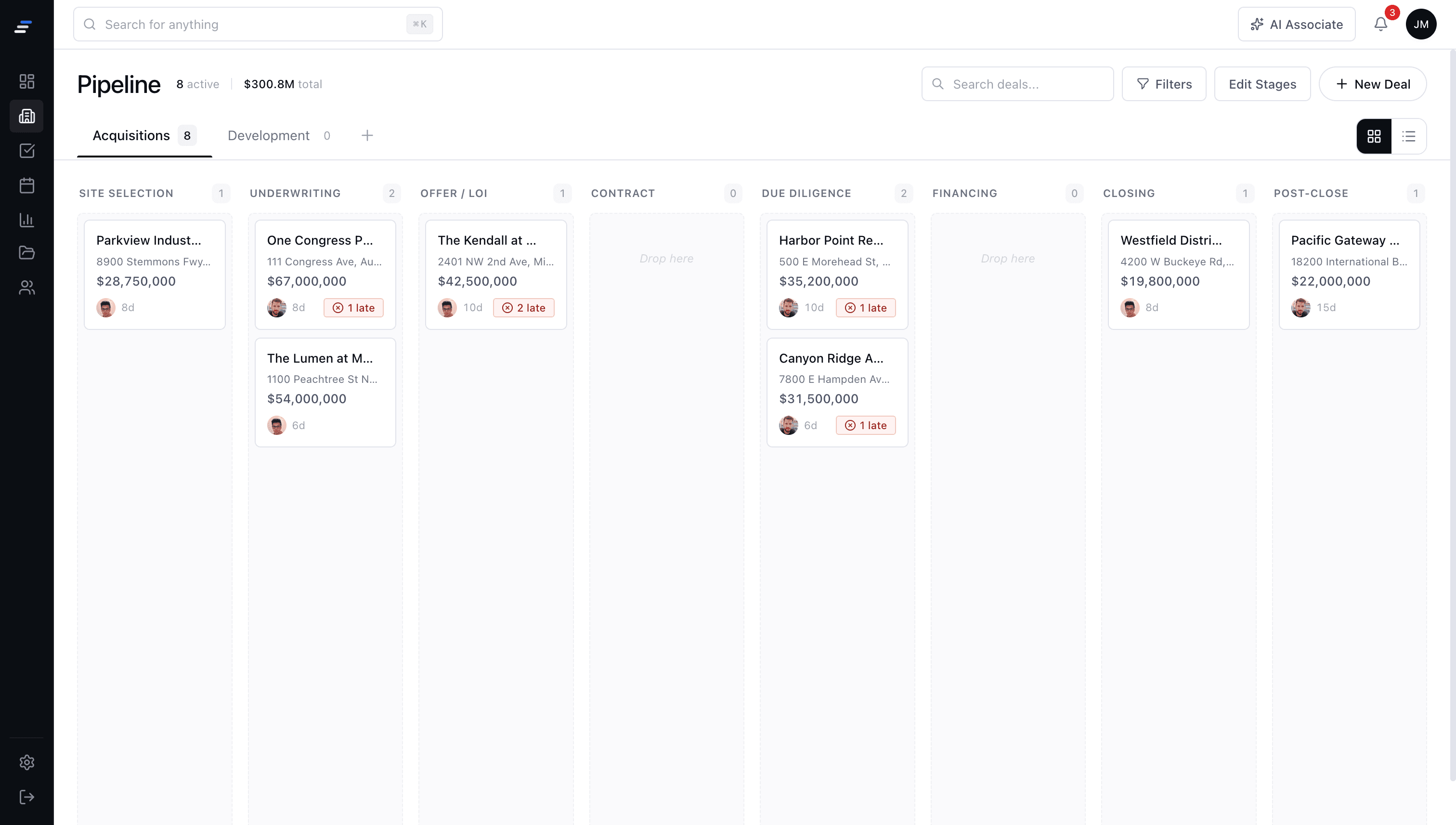

Pipeline

A CRE pipeline, done right

Every deal has a workspace, every workstream has an owner, and the pipeline is a live view into the team's actual work.

What belongs in a CRE IC memo

The sections below are the durable core of an institutional CRE IC memo. Adapt them for your firm's template but do not drop them.

1. Executive summary

One page. The deal name, asset class, purchase price, target return, key metrics, and the recommendation. If the committee reads nothing else, this is what they get. It should be written last so it reflects everything else in the memo.

2. Investment thesis

Why this deal, why this market, why this asset, and why now. Three to four paragraphs. The thesis is what the committee will hold the team accountable to when the deal is reviewed two years later.

3. Property overview

Location, building characteristics, unit count or square footage, tenant profile (if applicable), historical performance, and current condition. Include a site map, a satellite image, and interior photos if you have them.

4. Market analysis

Submarket fundamentals, comparable sales, rent comparables, demographic trends, and forward-looking supply and demand indicators. Use actual data, not broker narratives.

5. Financial underwriting

The pro forma, sensitivity analysis, key return metrics (IRR, MOIC, cash on cash, cap rate on year one and year five), and the assumptions behind them. Call out the assumptions that matter most. If the deal is sensitive to a 5 percent rent growth assumption, say so plainly.

6. Financing structure

Loan terms, lender, rate, amortization, loan to value, debt service coverage, and any unusual terms. Include the status of the lender conversations and the expected closing timeline.

7. Due diligence summary

A concise summary of what each workstream found. Financial DD confirmed the rent roll. Physical DD identified deferred maintenance items totaling $X. Environmental came back clean. Legal identified one title exception that has been resolved. If something has not been completed, say so and explain the timeline.

8. Risks and mitigations

The two or three risks that could hurt the deal and how the team plans to manage them. If the team cannot think of two or three risks, the memo is incomplete.

9. Recommendation and requested action

One paragraph. The amount of capital the team is asking for, the timeline, and the specific approval the committee is being asked to grant.

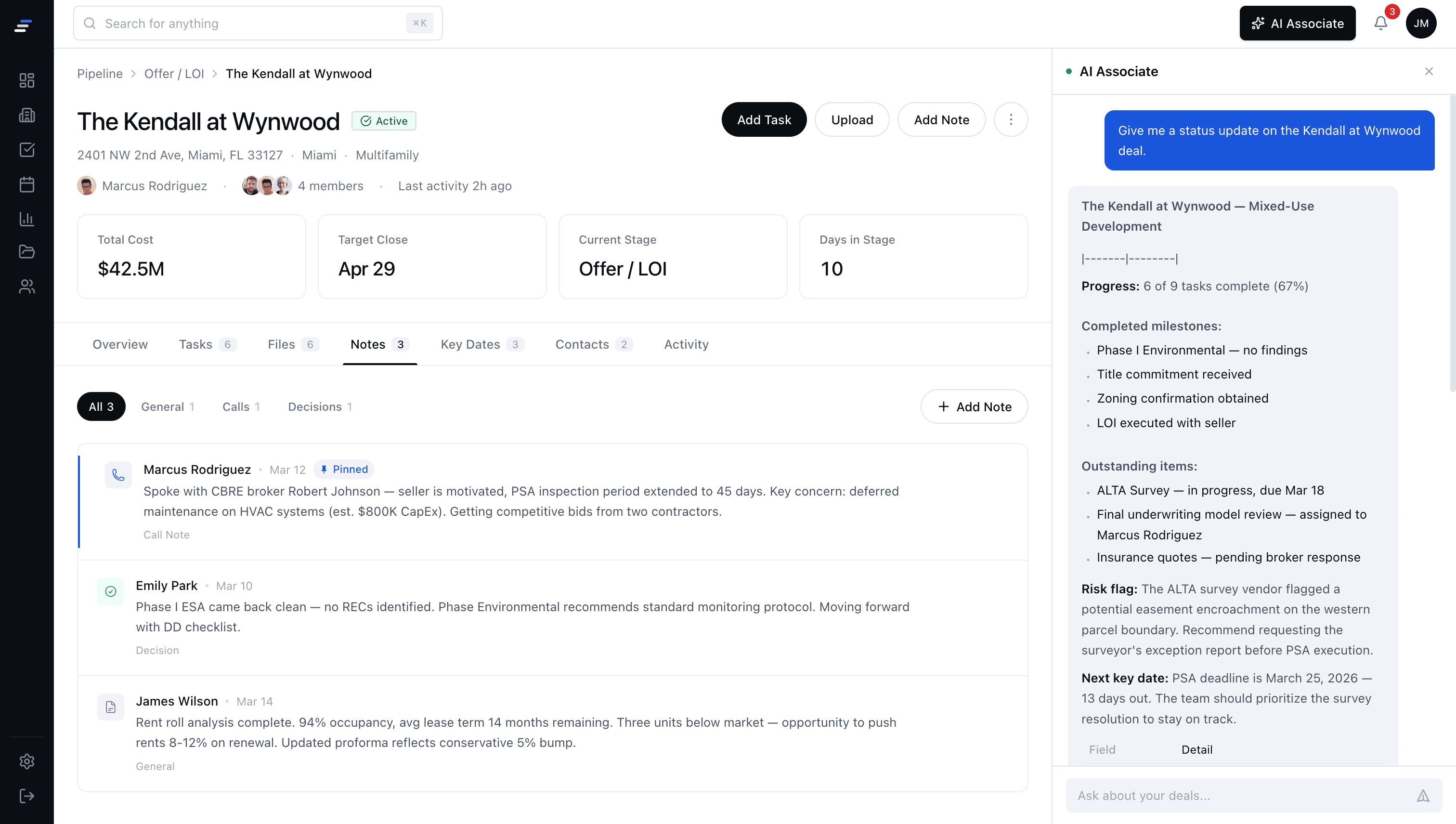

How MotionCRE supports IC memo workflows

MotionCRE does not generate IC memos for you. It does make the underlying data current and accessible so that when you write the memo, the numbers are right and the DD findings are complete.

Every deal has a workspace with the underwriting model, the DD workstream tasks, the financing quotes, the document library, and a running notes log. When the analyst sits down to write the memo, they have one place to pull from. The economics reflect the latest model. The DD summary reflects the latest workstream status. The financing section reflects the latest lender quote. The memo goes together in hours instead of days, and the version the committee reads matches the version of the deal the team is actually working on.

The AI Associate can draft an IC memo outline from the deal workspace, filling in the sections above from the documents, tasks, and data already in the deal. The draft is a starting point that the analyst reviews and rewrites in the team's voice, not a finished memo. The goal is to cut the mechanical assembly time so the analyst can spend more time on the analytical narrative.

Common questions

Executive summary, investment thesis, property overview, market analysis, financial underwriting, financing structure, due diligence summary, risks and mitigations, and the recommendation with requested action. The memo should reflect the current state of the deal workspace, not a frozen snapshot.

Join CRE teams already running their deals on MotionCRE

Your pipeline, your deals, tracked from sourcing to close.

14-day free trial · Full access · Cancel anytime